When a debtor makes a payment, it is important to update the ledger immediately to reflect the payment. An accounts receivable aging report is a report that shows the unpaid invoice balances of debtors along with the duration for which they’ve been outstanding. Most companies use the ageing of accounts receivable to monitor accounts receivable and optimise cash flow. Another method is to use the average collection period.

For this unit, the focus is on the ageing method.

Ageing analysis involves the classification of accounts receivables according to their age in days. This is to differentiate the customers’ account balances to meet the receivables turnover of the business.

Accounts are grouped according to their age. Problems in individual accounts can be detected through the analysis of receivables by ageing. A receivables ageing classifies customers’ accounts into amounts that are 0-30 days old, 31-60 days old, 61-90 days old, etc. Each classification is assigned a percentage of uncollectible based on company experience or industry standards.

The longer an account is past due, the more serious the problem. These can be identified quickly by ageing, and corrective action can be initiated promptly. This makes the monitoring relatively easier.

(Source: BizMove: How to Extend Credit to Customers)

The following is an illustration of the ageing of accounts receivable for T Murphey Pty Ltd as at 31 August 2021

Aged receivables summary

T Murphey Pty Ltd as at 31 August 2021

| Contact | Current | < 1 Month | 1 Month | 2 Months | 3 Months | Older | Total |

|---|---|---|---|---|---|---|---|

| Basket Case | - | - | 914.55 | - | - | - | 914.55 |

| Bayside Club | - | - | 3,434.00 | - | - | - | 3,434.00 |

| Boom FM | - | - | 1,650.00 | - | - | - | 1,650.00 |

| City Limousines | - | - | - | - | 599.50 | 250.00 | 849.50 |

| Cube Land | 495.00 | - | - | - | - | - | 495.00 |

| DIISR - Small Business Services | - | - | 4,200.00 | 3,850.00 | - | - | 8050.00 |

| Jack Blend | - | - | - | 445.50 | - | - | 445.50 |

| Marine Systems | - | - | - | 396.00 | - | - | 396.00 |

| Pinnacle Management | - | - | 3,080.00 | - | - | - | 3,080.00 |

| Ridgeway University | - | - | - | 6,187.50 | - | - | 6,187.50 |

| Total | 495.00 | - | 13,278.55 | 10,879.00 | 599.50 | 250.00 | 25,502.05 |

Businesses should evaluate the ageing of accounts receivable on a regular basis. The presence of an aged balance indicates the account should be followed up. Generally, the older the unpaid sales invoice, the less likely it is that the whole amount will be collected.

Unpaid invoices impact every aspect of a business. If cash flow is interrupted, there may be insufficient money to keep the business operational. Unpaid invoices need immediate attention; however, it is important when contacting customers to find out the reason an invoice is unpaid and follow correct procedure.

Customers may not have paid for different reasons. Most of the time, having a polite and professional conversation with your customer can help clear up any misunderstanding and assist in getting the invoices paid.

Invoice disputes

An invoice discrepancy occurs when there is a mismatch between the system-generated invoice and a customer’s records. Discrepancies may be in terms of quantity or value:

- Items invoiced have not been received by the customer.

- Incorrect goods were received by the customer.

- Items invoiced have the wrong quantity or amount.

- The customer is not happy with the goods or services.

- The customer asks why they have been billed this time.

- The customer says they cannot pay.

To understand what took place, you have to understand what happened within the accounts receivable at the invoice matching stage.

| Discrepancy | Possible Resolution |

|---|---|

| Items invoiced have not been received by the customer | Do a status check on the progress of the goods and make sure that the goods are delivered to the customer as soon as possible if delivery is in transit. If the goods are not scheduled to be delivered shortly, ask the customer to return the invoice to you. |

| Incorrect goods were received by the customer | Determine where the mistake occurred and the costs pertinent to augmenting the situation. Check on the possibility that another customer might have received incorrect goods as well, and make sure that the customer will receive the correct goods as soon as possible. |

| Items invoiced have the wrong quantity or amount |

Quantity : If the invoice quantity is incorrect, make the change by editing the invoice recorded in the sales journal or by sending a credit note to the customer. Value or Amount : If the invoiced amount is incorrect, make the change by editing the invoice recorded in the sales journal or by sending a credit note to the customer. |

| The customer is not happy with the goods or services | Come up with a compromise to decide how the situation could be resolved. Ask the client about their expectations and how you can fix it. Cross-check client expectations with client orders. Ensure you have the authority to authorise the proposed resolution. |

| The customer asks why they have been billed for time | Tell your client upfront that they will be billed for time and make sure to track the time through timesheets and the pricing. Provide the client with a copy of your policy and procedure, which outlines the time intervals clients will be billed for. |

| The customer says they cannot pay | Try to produce a resolution by suggesting a payment plan. If this is not feasible, pass the invoice to a credit collector. |

Steps for tackling invoice disputes

- Attach supporting documents such as sales orders to customer invoices for easier double-checking.

- Make follow-up calls once an invoice has been sent to a customer. This is to ensure that they received the invoice. Take this time to confirm the details on the invoice.

- For consistency, ensure the accounts receivable department has a documented policy and procedure for dealing with outstanding invoices.

- Use invoicing software for easier tracking and monitoring.

- Offer live chats to your customers in cases of disputes.

Customer deductions errors

Businesses provide goods and services to their customers and invoice them at agreed rates. In some cases, customers remit less than the invoiced amount due to withholding part of the payment. Amounts withheld are called deductions. In most cases, customers will take deductions only when there is a legitimate problem with an invoice. If they do take a deduction in error, they are generally willing to pay once the error has been proven to them.

Common reasons for deductions include such things as pricing errors, quantity errors, delivery problems (too early, too late, to the wrong location, not signed for), concealed shortages, the wrong product shipped, returns for credit, rebates, advertising credits, etc. None of these deductions is initiated by the accounts receivable department. However, it is the accounts receivable department responsible for identifying and rectifying the issue so that the accounting records are correct.

Erroneous deductions

Some customers may take deductions because they simply lack the information needed to process payment. Others may use this as a tactic to slow payment or hope the issue will just end up as a write off by a weary or disorganised seller.

The unfortunate fact is that the time and cost to research and resolve a deduction can be significant. If it is ultimately determined that the deduction was taken in error, the effort, time and expense required to document your position can be significant. If the amount is found to be due and payable, additional effort will still be required to convince the customer to pay the disputed amount.

Steps for tackling deduction errors

- Determine if there is a return on your time and effort invested (ROI) to pursue a small dollar deduction.

- Analyse and document.

- If the customer is making claims without supporting documentation, ask them to immediately provide what you need.

- Focus on reducing the volume and impact of deductions.

- Build a minimum dollar threshold into your credit collections policy for collection versus write-off.

- Decide whether to chargeback or not.

- Determine how the customer is treating others in the marketplace.

- Have a good system to automate the deduction management process.

(Source: Credit Today: Managing the Customer Deduction Challenge)

Methods of correcting errors

It is important errors are corrected in the same accounting period the error was made; otherwise, the final accounts, Profit & Loss and Balance Sheet, will not show the true financial position of the business. Errors can be corrected by adjustment notes, delay credits or refunds.

An adjustment note, also known as a credit note, is a posting transaction that can be applied to a customer’s invoice as a payment or reduction.

A delayed credit is a non-posting transaction that you can include later on a customer’s invoice.

A refund is a posting transaction that is used when reimbursing customer money.

Although all customers must meet the credit requirements of a business before credit is approved, inevitably, some accounts will always become uncollectable. For example, a customer may not be able to pay his outstanding invoices because he is a sole trader and has no income due to a workplace accident.

- Bad debt: Bad debts are account receivables that are clearly not collectable. These are account receivables that have been recorded for a long period. Once identified, bad debts are no longer considered an account receivable and become a loss.

- Doubtful debt: A doubtful debt is an account receivable that could become a bad debt. These are credit entries made in a separate account that is made for doubtful debts.

Bad debts can be written off using either the allowance method (sometimes referred to as the provision method) or the direct write off method.

Direct write off method

Using the direct write off method, a business recognises the bad debt expense when it is certain that the invoice will not be paid. The journal entry is a debit to the bad debt expense account and a credit to the accounts receivable control account. If using the accrual accounting method, it may also be necessary to reverse any related GST that was charged on the original invoice, which requires a debit to the GST Collected account.

| Bad debts expense | $1,000 | |

| GST collected | $100 | |

| Accounts receivable CONTROL ACCOUNT (To write off M Mar account as bad debt) |

$1,100 | |

| Subsidiary ledger entry | ||

| Accounts receivable Subsidiary Account M Mar (To write off M Mar account as bad debt) |

$1,100 |

Note: The credit to Accounts Receivable must be recorded in both the General Ledger control account and the subsidiary ledger.

Under the direct write off method, the bad debt expense is often recorded in a different accounting period than when the original invoice was recorded. It is not until the accounts receivable have been outstanding for a period of time that it becomes apparent that it is uncollectible.

This means that when the loss is reported as an expense in the accounts, it’s being matched against revenue on the income statement that’s unrelated. This results in total revenue is incorrect in both the period the invoice was recorded and the period when the bad debt is expensed.

Allowance method

The allowance method provides a more accurate picture of the amount of accounts receivable expected to be collected at the end of a reporting period.

The first step in the allowance method is for the business to make an adjusting entry at the end of the accounting period for bad debts that they expect in the future. This allowance can be based on a percentage of net sales method or the ageing of receivables method. By creating the allowance, the bad debt expense is being recognised against sales within the same accounting period.

The allowance for doubtful debts is an estimate of the amount of accounts receivable that are expected to become uncollectible. As the business does not know which customers this will be, it uses a contra account instead of a direct credit to the accounts receivable account

June 30, 2021

| Bad debts expense | $1,000 | |

| Allowance for doubtful debts | $1,000 | |

| (To estimate the bad debt expense) | ||

The Allowance for Bad Debts is a contra-asset account of Accounts Receivable. It is presented in the balance sheet as a deduction from the gross accounts receivable amount.

When the company decides to write off a bad debt, it does so by debiting the allowance for doubtful debts accounts and crediting accounts receivable control account.

| Allowance for doubtful debts | $1,000 | |

| GST collected | $100 | |

| Accounts receivable CONTROL ACCOUNT (To write off M Mar account as bad debt) |

$1,100 | |

| Subsidiary ledger entry | ||

| Accounts receivable Subsidiary Account M Mar (To write off M Mar account as bad debt) |

$1,100 |

Note: The credit to Accounts Receivable must be recorded in both the General Ledger control account and the subsidiary ledger.

In case the allowance for bad debts is over or understated, the entries are as follows:

| Allowance for doubtful debts | $XX | |

| Bad debts expense | $XX |

| Bad debts expense | $XX | |

| Allowance for doubtful debts | $XX |

Percentage of Sales method

The percentage of sales method estimates uncollectible accounts from a given period's credit sales. In theory, the method is based on the percentage of the actual uncollectible accounts of previous years compared to the sales of previous years. This method is used by some businesses for monthly reporting; however, for year-end reporting, the ageing of receivables method should be used.

Bad debt expense = Net sales (total or credit) × Percentage estimated as uncollectible

The percentage-of-sales method formula to determine the amount of the ending estimated bad debts entry

Ageing of Receivables method

The ageing of receivables method involves preparing an ageing schedule in which customer’s accounts receivable balances are grouped depending on the length of time they have been outstanding. Once the accounts have been aged, the expected bad debt is calculated by applying percentages based on past experience to the totals of each group. The estimated percentage of uncollectible debt increases as the number of days the debt is outstanding increases.

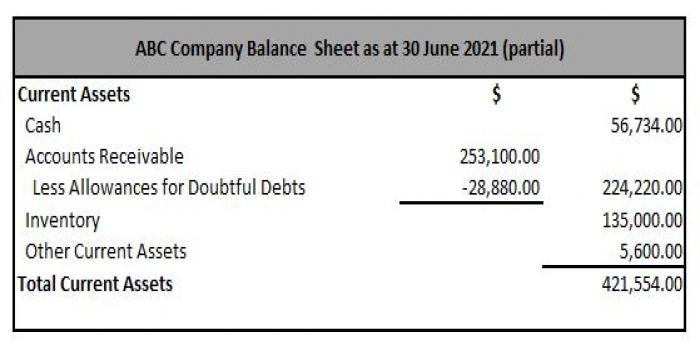

Example using the ageing of receivables method

Below is the ageing schedule for ABC Company. The total estimated bad debts for ABC Company is $36,880.00, being the accounts receivable expected to become uncollectible in the future. This amount represents the required balance of the Allowance for Doubtful Debts on the 30 June 2021.

| Age | Amount $ | % Uncollectible | Allowance for bad debts |

|---|---|---|---|

| 0–30 days | $109,000.00 | 2% | $2,180.00 |

| 31–60 days | $64,000.00 | 4% | $2,560.00 |

| 61–90 days | $44,900.00 | 10% | $4,490.00 |

| 91–120 days | $30,200.00 | 75% | $22,650.00 |

| Over 120 days | $5,000.00 | 100% | $5,000.00 |

| Totals | $253,100.00 | $36,880.00 |

The adjusting entry on 30 June 2021 is the difference between the required balance and the existing balance of the Allowance for Doubtful Debts account.

The existing balance of the allowance for doubtful debts account is $28,880. To bring the account to a credit balance of $36,880, equal to the estimated bad debt in the ageing schedule, the allowance for doubtful debts needs to be increased by $8,000.

The journal entry to increase the allowance is:

| Date | Details | Debit | Credit |

|---|---|---|---|

| 30/06/2021 | Bad debt expense | 8,000 | |

| Allowance for doubtful debts | 8,000 | ||

| To adjust the allowance account to total estimated uncollectible | |||

Recovered bad debts

If a bad debt is recovered, two journal entries are prepared to reverse the write-off entry and to record collection, respectively. For example, in the case of the illustration above, out of the $36,880, $2,000 was recoverable.

| General ledger entry | |||

|---|---|---|---|

| Dr | Cash | $2,000 | |

| Cr | Accounts receivable control account Cash received from accounts receivable previously written off |

$2,000 | |

| Dr | Accounts receivable control account | $2,000 | |

| Cr | Bad Debts Recovered Bad debt previously written off recovered |

$2,000 | |

Sometimes a business might only be able to recover part of a debt. This means the unrecoverable amount only has to be written off.

There are internal processes that a business can adopt which will reduce its risk of incurring bad debts. These include:

- Credit check on all new customers before credit is offered

- Potential credit customers fill out a credit application form

- Send invoiced promptly, preferably with the goods

- Send regular (monthly) statements to customers promptly

- Follow up overdue payments promptly

- Maintain a history of credit dealings with each customer

- Ensure that all employees are familiar with the company’s credit policy

- Revise the company’s credit policy periodically to document the process for:

- When is an Aged Receivables account deemed to be a bad debt?

- When the customer has filed for bankruptcy

- When the debtor has left the country or cannot be traced

- When the debt is too small to be worth pursuing

Section 25-35 of the Income Tax Assessment Act 1997 and Taxation Ruling TR 92/18 sets out the circumstances and conditions in which a deduction for bad debts will be allowable.

Deductions for unrecoverable income (bad debts)

Your company will also have policies and procedures to guide you in the process of:

- dealing with overdue accounts

- verifying whether debts are doubtful or bad

- how you report and document bad and doubtful debts

- when bad debts are to be written off

- who can authorise the write off of bad debts?

Circumstances, when a debt can be written off could include:

- If the debtor is bankrupt, receivable or liquidated. The debt is written off until the funds are available.

- Where the debtor moved the address and failed any attempts to locate it.

- If the recovery action is not economical due to the relatively small value of the debt and/or the potential cost of recovery is more than the initial debt.

- If a particular debtor's medical, financial or domestic circumstances do not warrant recovery or further recovery action at that time.

- Where legal proceedings through the courts have proved unsuccessful or on legal advice.

- Where the collection agents advise that it is no longer cost-effective to pursue the debt.

Writing off bad debts in a computerised accounting system

In computerised accounting systems like Xero and MYOB, a bad debt is written off by first creating a credit note (Adjustment Note) and then applying the credit note to the customer’s outstanding invoice/s.

Writing off bad debts – MYOB AccountRight

Read the City of Prospect’s Accounting Policies and Procedures Manual.

Locate the information on Debt Collection and complete the following.

Assume that Twin Peaks Intrepid Travel have decided to adopt the following as their credit policy.

Credit Policy and Procedures

This credit policy must be agreed to in writing by all customers before credit sales are allowed.

Credit limit of $3000 per customer.

The customer is sent an invoice for transaction(s) at the end of the month of purchase(s).

Payment is expected within 30 days of that invoice being sent.

Procedures if customer has any amounts

- 1 month overdue: A copy of the overdue invoice is sent out (with the invoice for any subsequent purchases made that month if there are any) with an “Friendly Reminder” sticker on it.

- 2 months overdue: A copy of the overdue invoice is sent out (with the invoice for any subsequent purchases made that month if there are any) with an “Final Notice” sticker on it.

- 3 months overdue: A telephone call is made to the customer, asking the reason for non-payment of the invoice(s) and when payment can be expected. A debt recovery plan can be discussed with the customer, for example an extended payment date or a negotiated payment schedule.

- Over 3 months overdue: A telephone call is made informing the customer that their credit facility will be put on hold unless payment is received immediately. No more credit is to be extended to this customer until the account has been settled. A letter of demand is to be sent to the customer

- Over 4 months overdue: For accounts with amounts under $250.00 owing, they will be considered bad debts and written off. For accounts with amounts over $250.00 owing the customer’s account will be turned over to a collection agency.

In the attached Excel Workbook Prepare an Aged Receivables Summary Report as at 31 January 2021 using the following dates to age the debtors.