Welcome to your next module - Process financial transactions and extract interim reports.

In this module, you will be presented with the knowledge required to understand the fundamentals of financial reporting and systems used to manage accounts.

The knowledge covered in this module is included but not limited to:

- Check and verify supporting documentation

- Prepare and process banking and petty cash documents

- Prepare and process payable and receivable invoices

- Prepare journals

- Update financial data and systems

- Prepare deposit facility and lodge flows

- Finalise trial balance and interim reports.

Throughout this module, you will be presented with activities. These activities have been designed to test your comprehension of key concepts and review what has been covered in the topic.

Learning Checkpoint

After each topic, you will have the opportunity to engage with learning checkpoints. These learning checkpoints will allow you to test your understanding of the topic before undertaking the assessment. Solutions to the learning checkpoints are provided; however, we encourage you to attempt the activity before viewing the answer. If you have questions regarding your answers and/or the solutions provided, contact your trainer.

Case Study

At the end of this module, you will be required to undertake assessments assuming the role of a Junior Accounting at Ace Finance.

Learning objectives

After you have completed this topic, you should have knowledge of:

- What is accounting and bookkeeping

- Different types of business entities and their reporting requirements

- Accounting and bookkeeping professional bodies in Australia

- GAAP

- Accounting Concepts

- Accounting Conventions

- Accounting Standards

- Accounting Policies and Procedures

Accounting is the process of recording, classifying, summarising and interpreting financial data. Businesses use accounting to keep their financial information organised, understand their current financial position, stay compliant and meet their reporting requirements.

Bookkeeping is the process of methodically gathering, recording and reporting financial information to explain the overall health of a business. Bookkeeping answers questions like:

- How profitable is the business?

- How much money does the business owe to lenders?

- How much money do customers owe to the business?

- How much money does the business owe to suppliers?

- How much tax needs to be paid?

![]()

The person who is responsible for maintaining the day-to-day financial transactions in a business is known as the bookkeeper. Accountants rely on the work done by the bookkeeper. They review the financial records and statements for decision making, planning and controlling the business. For example:

- Investment decisions

- Budgeting

- Performance measurements

Accountants are able to provide insights about the company’s overall health based on the financial reports provided by a bookkeeper.

Bookkeepers and Accountants

While both accountants and bookkeepers play a role in managing a business’s finances, they each support the business in different ways and perform various financial processes. The table below outlines the main differences between bookkeepers and accountants.

| BOOKKEEPER | ACCOUNTANT | |

|---|---|---|

| CREDENTIALS |

No formal education is required. However, there are basic skills you need to have to succeed:

Often these skills are acquired through completing a Certificate IV in accounting and bookkeeping qualification. Certificate IV in Accounting and Bookkeeping is currently cited as meeting the TPB education requirements for registration. |

Formal qualification - Bachelor's degree in accounting or finance. |

| FUNCTIONS | Bookkeepers record and manage the daily financial transactions of a business. This includes:

|

Accountants provide financial analysis on data that has been entered by a bookkeeper. This includes:

|

| DOCUMENTATION PREPARED | Bookkeepers prepare:

|

Accountants prepare:

|

| REPORTING OBLIGATIONS | Bookkeepers lodge:

|

Accountants lodge:

|

| PROFESSIONAL CERTIFICATION | Bookkeepers can become members of:

|

Accountants can become members of:

|

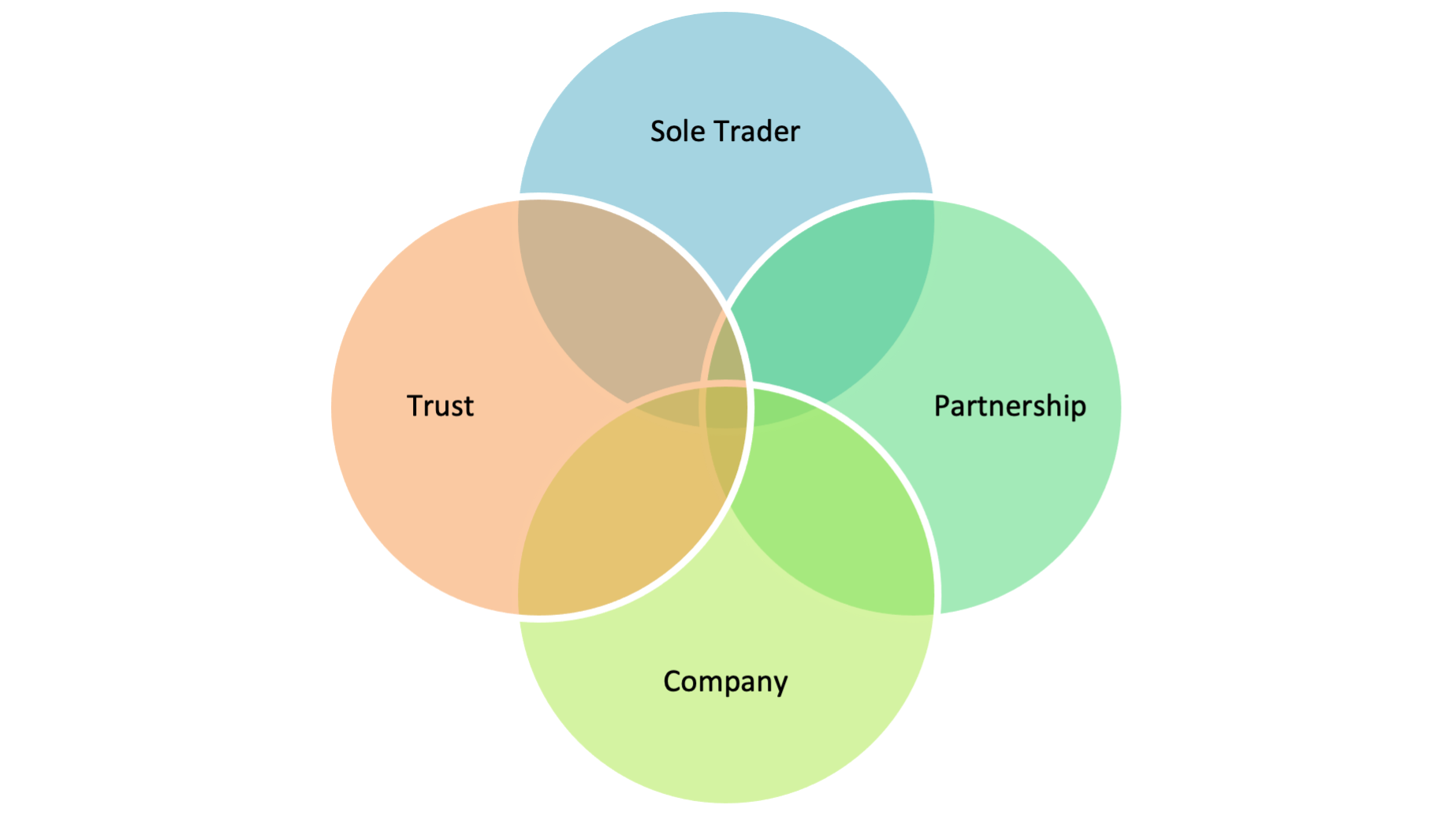

One of the key decisions a business owner must make prior to commencing the business is the organisational structure of the business. In Australia, there are a number of business structures an owner can choose from, including:

- Sole Trader

- Partnership

- Company

- Trust

Business Types

Let’s examine each of these business types in more detail.

Sole Trader

A sole trader is a self-employed person who owns and runs their business as an individual.

- It is the simplest and cheapest business structure.

- Sole traders have only one owner who controls and manages the business.

- The owner is legally responsible for all aspects of the business, including debts and losses.

- The owner can employ workers in their business; however they can’t be an employee of their own business.

- The owner is responsible for paying super for any workers they employ. They may also choose to contribute super for their own retirement into a super fund.

- Sole traders pay the same tax as individual taxpayers according to the marginal tax rates.

Watch this short video to understand the advantages and disadvantages of being a sole trader.

To find out more about a Sole Trader Business Structure, click here

Partnership

- A partnership is a business structure where two or more people own and control the business.

- A partnership is relatively inexpensive to set up and operate.

- All partners share income, losses and control of the business.

- Partnerships are governed by the Partnership Act in each Australian State.

- A partnership agreement can help prevent misunderstandings and disputes about what each partner brings to the partnership and what they are entitled to receive from the business.

- The partners in a partnership cannot be employees of their own business.

- The partnership can employ workers in their business and is responsible for paying super for any workers they employ

- Partners are responsible for their own superannuation arrangements

Watch this short video to understand the advantages and disadvantages of operating as a partnership.

To find out more about a Partnership Business Structure, click here

Company

A company is a business entity run by its directors and owned by its shareholders.

- Companies have higher setup and administration costs.

- While a company provides some asset protection, its directors can be legally liable for their actions and, in some cases, the debts of the company. All directors of a company are required by law to verify their identity and get a director identification number. Click here for information on Director ID.

- Companies are regulated by the Australian Securities & Investments Commission (ASIC). Watch this short video to understand the advantages and disadvantages of operating a business as a company.

- Companies have additional reporting requirements.

To find out more about a Company's Business Structure, click here

Trust

Setting up a trust can be expensive as a formal deed is required outlining how the trust will operate

- A trustee is legally responsible for the operation of the trust.

- There are formal yearly administrative tasks for the trustee of the trust

- The trustee can be an individual or a company.

- Profits from the trust go to beneficiaries.

Watch this short video to understand the advantages and disadvantages of operating a business as a trust.

To find out more about a Trust Business Structure, click here

In Australia, the practice of accounting is influenced by three professional accounting bodies: the Institute of Chartered Accountants in Australia (CA), the Australian Society of Certified Practising Accountants (CPA Australia) and the Institute of Public Accountants (IPA).

In addition to this, there are two main professional bookkeeping bodies, The Institute of Certified Bookkeepers (ICB) and the Australian Bookkeepers Network (ABN).

Bookkeeping professional bodies

| Bookkeeping Body | Membership | Website |

|---|---|---|

|

The Institute of Certified Bookkeepers (ICB) |

ICB have different levels of membership. Student membership is for anyone currently studying to become a bookkeeper. The membership is for a 2-year period with progression to Affiliate member once the qualification is complete. The minimum education requirement for Affiliate membership and above is:

|

Institute of Certified Bookkeepers (icb.org.au) |

|

Australian Bookkeepers Network (ABN) |

ABN members must:

|

Bookkeeping Australia | Australian Bookkeepers Network (austbook.net) |

Accounting professional bodies

|

Certified Practicing Accountants (CPA) |

CPA’s must:

|

Home | CPA Australia |

|

Charted Accountants Australia & New Zealand (CA) |

Chartered Accountants:

|

Chartered Accountants Australia & New Zealand | CA ANZ (charteredaccountantsanz.com) |

|

Institute of Public Accountants (IPA) |

An IPA accountant:

|

Institute of Public Accountants |

For students who are/ have studied accounting overseas and are wanting to come into Australia and become an accountant, there are some options for you.

Before we start to examine the accounting process, it is important to understand the framework within which the accounting process operates.

GAAP Principles

Underlying accounting, there are agreed principles, concepts and accounting standards. These have been developed over time to provide a uniform, standardised system of accounting by which companies can be compared based on their performance and value.

These principles, which serve as the rules of accounting for financial transactions and preparing financial statements, are known as ‘Generally Accepted Accounting Principles,’ or GAAP. By applying the GAAP principles, accountants can ensure that financial statements are both reliable and informative.

GAAP involves both accounting concepts and accounting conventions.

Accounting Concepts

Some of the most fundamental accounting concepts are:

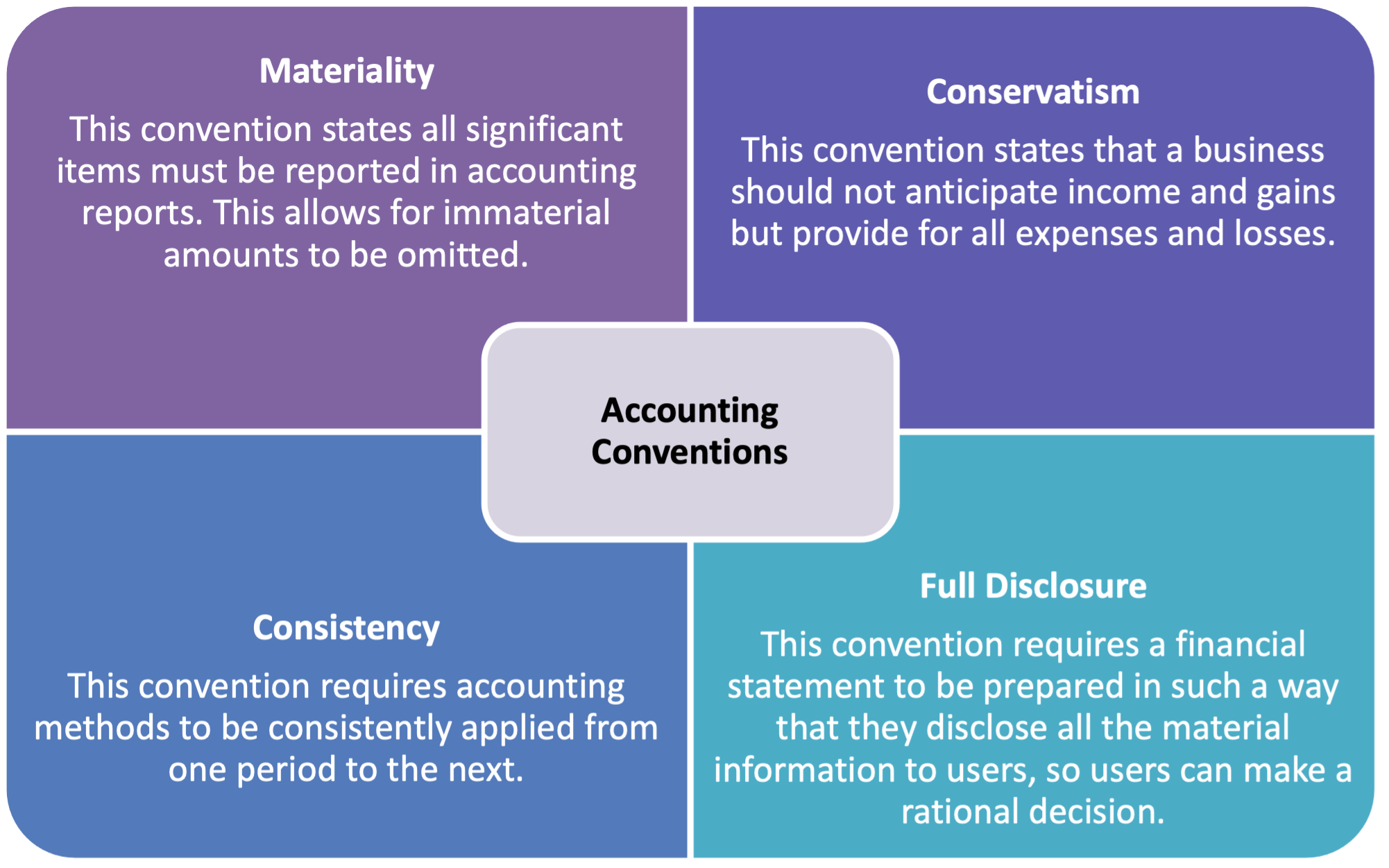

Accounting Conventions

Accounting conventions are guidelines for complicated and unclear business transactions. They are not compulsory or legally binding; however, they have generally accepted principles and maintain consistency in financial statements. There are four main conventions materiality, conservatism, consistency and full disclosure.

To read more about Accounting Conventions, click here.

Accounting Standards

Accounting standards are policy documents that provide specific direction for accountants and other advisers in the required accounting measurements and disclosures for types of material transactions and events.

These accounting requirements affect the preparation and presentation of an entity's financial statements. Both CA and CPA Australia have played a significant role in the development of these accounting standards

The accounting standard in Australia are regulated by the Australian Accounting Standards Boards (AASB).

The AASB responsibilities include:

- developing a conceptual framework for the purpose of evaluating proposed standards

- making accounting standards under section 334 of the Corporations Act 2001

- formulating accounting standards

- contributing to the development of a single set of accounting standards for worldwide use

- advancing and promoting the main objects of Part 12 of the ASIC Act.

To access more information on the Australian accounting standards, click here.

Reporting Requirements

Australia has different financial reporting requirements for different types of entities. This is mainly based on the level of public interest in the entity. Types of entities that need to prepare financial reports can be classified as:

- disclosing entities (mainly listed corporations and registered managed investment schemes/prescribed interest undertakings) that have listed securities or have issued shares and other securities as a result of the circulation of a prospectus.

- unlisted public companies and large proprietary companies (that is, a proprietary company that meets at least two of the following criteria: gross operating revenue of $10 million or more, gross assets of $5 million or more and 50 or more employees)

- small proprietary companies.

Under the Corporations Law, all disclosing entities, companies and registered managed investment schemes are required to maintain records that accurately record their financial transactions, which would enable the preparation of financial statements and the audit of those financial statements.

Annual financial statements must be prepared by all entities except small proprietary companies. The annual financial statements consist of a:

- Balance Sheet

- Profit and Loss Statement

- Cash Flow Statement.

Information that needs to be disclosed in the financial statements is contained in accounting standards and have the force of law under the Corporations Law.

Business Policies and Procedures

Policies and procedures are essential tools for both managers and staff. When a workplace has a set of policies and procedures, staff does not constantly have to make decisions about what to do. Written policies and procedures empower staff to perform their duties consistently and systematically, reducing the occurrence of human errors. Furthermore, they provide management with some assurance that the work and actions of their staff are compliant with industry regulations and guidelines.

Accounting policies are important to any business to maintain consistency and to set up a standard for decision-making. Accounting policies are usually approved by top management and do not change much throughout the years. They are developed for long-term use, reflecting an organisation's values and mandatory requirements.

Accounting policies and procedures should also be regularly reviewed and updated. As organisations change in size and complexity, implement new systems, or are subjected to changes in regulations or accounting standards, their existing policies and procedures will need to be modified.

Employees should be fully conversant with the organisation's accounting policies and procedures so when they encounter a situation that they are unsure about, they can reference the relevant policy or procedure to verify the correct way to deal with the situation.

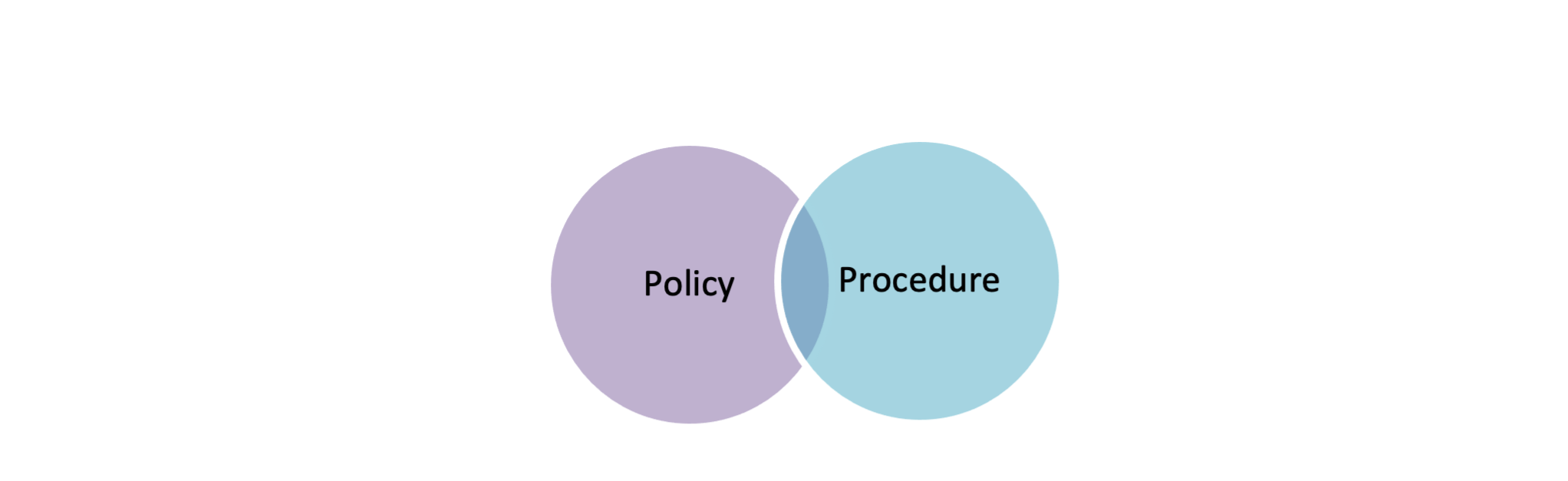

What is a policy?

A policy is a statement that describes an organisation's views in regard to particular matters. It is a set of principles, or rules, that provide a definite direction for an organisation and embrace the general goals and acceptable procedures. In short, policies assist in defining what must be done when particular events occur.

What is a procedure?

A procedure is a clearly laid out, step-by-step method that shows workers how to implement an organisation's policies, responsibilities and work tasks in a correct and consistent manner.

Policies and procedures are usually compiled together to form a Policy and Procedures Manual, which is a compilation of the written records of the agreed policies and practices of an organisation. The manual should be maintained in a physical documentation system so that it can be updated and added to as policies and practices are reviewed and changed. Policy and procedure manual generally include the following financial policies and procedures:

- Credit policy and procedures

- Purchasing policy and procedures

- Invoicing policy and procedure

- Banking and cash handling policy and procedure

- End of period reporting policy and procedure

Now that we've looked at some of the assumptions and practices that create the foundations for accounting, we can now begin to look at the accounting process itself.

Therefore, all the transactions associated with a business must be separately recorded from those of the business owners or other businesses.

The accounting process involves:

- Identifying and analysing business transactions

- Recording in the journal

- Posting to the ledger

- Unadjusted trial balance

- Adjusting entries

- Adjusted trial balance

- Financial statements

- Closing entries

- Post-closing trial balance

Although it may seem logical to structure the learning so that it follows the accounting process illustrated above, in this module, we will introduce the accounting process in a different sequence, starting with an explanation of the Statement of Financial Position (Balance Sheet) and Statement of Financial Performance (Profit & Loss). We believe having a solid understanding of the components of the Balance Sheet and Profit & Loss Statement will help you understand the fundamentals of accounting and some of the more complex accounting concepts.