Australia has a progressive tax system which means the more income earned the more tax paid.

Based on the fundamental framework of a progressive tax system are a series of legislation and regulations which detail the requirements for recording and reporting financial activity. A business needs to register for GST if its annual GST turnover (essentially gross income) is $75,000 or more. Additional tax laws are specific to the type of business structure.

As a reminder, businesses in Australia can be structured as a:

- Sole trader- an individual running a business. This is the simplest and cheapest business structure.

- Partnership-a group or association of people who carry on a business and distribute income or losses among themselves.

- Company-a legal entity with higher setup and administration costs and additional reporting requirements.

- Trust -an entity that holds property or income for the benefit of others.

- Not-for-profit (NFP) - organisations that provide services to the community and do not operate to make a profit for its members (or shareholders, if applicable). The threshold for paying GST for this type of organisation is $150,00.00.

A note about NFP:If the business is a charity, it is exempt from income tax. To find out what is required to be considered a charity and additional specifics, please see the ATO website for current information.

Reporting and payment

To facilitate reporting and payment, all businesses must obtain a Tax file number before the application for the Australian Business Number (ABN), which is to be used in all business dealings.

Australia’s overall tax burden is relatively low compared to developed countries and regional competitors. The federal government raises around 81 per cent of total tax revenue in Australia. State and Territory governments receive 45 per cent of their revenue through transfers from the federal government, including all GST revenue.1

Why the tax system exists

The main objective of Australia’s taxation system is to raise revenue effectively and efficiently for redistribution to the community in accordance with government priorities.The current tax system raises over $400 billion for public services, such as health, social security, education, infrastructure, and defence. Most of its tax revenue comes from personal and corporate income taxes and taxes on consumption.

The taxes we all pay fund community services such as:

- health care

- education

- emergency services

- roads and train lines

- the Australian Defence Force

- welfare and disaster relief.2

Given that GST revenue and other taxes collected support the Australian economy, a BAS agent, bookkeeper or tax agent carries a burden of responsibility to describe, record, and advise these regulations accurately to the best of their ability. Understanding not just the requirements but the reasons for having them will help ensure your work in the field of accounting is competent and ethical. Doing right by your clients or the business you work for is literally written into the job requirements with their code of conduct, which will be discussed shortly.

The following topics cover everything you need to know about lodging a Business Activity Statement with the Australian Tax Office:

- Legislation and requirements

- Industry codes of conduct

- Review and apply GST

- Payroll activities

- Reconcile and prepare activity statement

- Lodge activity statement

- References and copyright

There are several roles that play a part in the government's effort to raise revenue effectively and efficiently for redistribution to the community.

Some bookkeepers call themselves accountants. Many accountants spend significant time doing bookkeeping. The terms ‘accounting’ and ‘bookkeeping’ overlap significantly. ‘Accounting’ can extend into technical areas that bookkeepers typically are not qualified or experienced in performing.

Sometimes accountants extend their influence into areas they are not suitably experienced or knowledgeable to provide. Fortunately, codes of conduct for members of professional associations unanimously require accountants and bookkeepers to ensure they DO NOT do work they do not know how to do.

The table below is provided as an overview. Each role has activities commensurate to their level of qualifying education and years of experience in the field.

| Role | Allowed to do |

|---|---|

| Self-employed bookkeeper | Data entry, accounts payable and receivable, bank reconciliation, run financial reports, run payroll (Not allowed to lodge statements) |

| Bookkeeper as an employee | All of the above, and lodge PAYG, FBT, Super, and BAS |

| BAS agent | All of the above plus BAS preparation and lodgment |

| Tax agent | All of the above plus income tax returns. |

Bookkeeper

Daily tasks that can be carried out by a bookkeeper are varied.

- Recording the financial transactions of a business in bookkeeping software (such as MYOB or QuickBooks), spreadsheets or databases.

- sales and purchases

- expenses and losses

- incomes and gains

- borrowing money

- buying products or raw materials for production.3

- Arranging payment of accounts.

- Preparing and sending invoices and receipts to debtors.

- Processing payroll and maintaining employee records.

- Carrying out bank reconciliations.

- Reporting for preparation of a Business Activity Statement (BAS).

- Checking figures and reporting for accuracy.

- Reporting any irregularities in data to management.

- Producing balance sheets, income statements and other financial documents.4

Bookkeeping involves a number of common business activities such as:

- issuing invoices and paying bills

- making wages and super payments

- preparing cash books (paper or electronic)

- preparing financial accounts – for example, profit and loss statements and balance sheets.

Bookkeepers provide a range of accounting services for employers or clients and may be responsible for tasks and functions such as:

- payroll

- data entry

- petty cash

- record keeping

- reconciling bank accounts

- accounts payable and receivable.

Why a bookkeeper is needed

Watch this five-minute video for an explanation.

The Institute of Certified Bookkeepers (ICB)

The organisation, ICB, promotes and maintains standards of bookkeeping as a profession by establishing relevant qualifications and awarding grades of membership that recognise academic attainment, working experience and competence.

A “Member” of the ICB (MICB) achieves certification by proving that they have performed bookkeeping services at a significant level for a period longer than two years.Members must have a Certificate IV in Accounting and Bookkeeping. This qualification recognises a bookkeeper’s skills and competence formally and, more importantly, is also recognised within the education system.

Knowledge, skills, and characteristics of Professional bookkeepers

- Knowledge of general accounting principles, relevant legislation and current best practices.

- IT general skills, especially in accounting software, online government portals and electronic payments.

- Consistency, reliability and trustworthiness.

- Honesty – particularly in reporting problems, gaps in knowledge requiring research or mistakes that may have been made.

- Professional code of conduct evidenced by a high standard of service and strong work ethic.

- Able to research and analyse problems in the accounts.

- Speed and accuracy in data entry and typing.

- Regular professional development and professional indemnity insurance.

Self-employed bookkeeper or bookkeeper employed by a business

If a bookkeeper is employed by a business, it is assumed that the business takes on any risk of poor advice, errors in information, or missed deadlines for lodging with the ATO. It is likely that the business also employs an Accountant, who is ultimately responsible for the integrity of their bookkeepers activities. However, if a bookkeeper is offering their own services for a fee or reward, then the government limits their services in or der to protect consumers.

Registered Tax and BAS agents

Tax and BAS agents may provide all of the services of a bookkeeper (though they are often separate roles) and give advice and services about:

- GST

- fuel tax

- luxury car tax (LCT)

- wine equalisation tax (WET)

- fringe benefits tax (FBT - collection and recovery only)

- pay as you go withholding (PAYG)

- PAYG instalments (PAYGI)

Tax agents can also:

- provide advice about, prepare and lodge income tax returns.

Scope of services (BAS agent vs Tax agent)

A registered BAS agent, under the Tax Agent Services Act, provides advice services for a fee or reward. BAS agents are authorised to prepare and lodge BAS returns, including GST and PAYG withholding. However, paid employees that provide BAS services on or behalf of their employers, do not need to be registered.

The main limitation of a BAS agent compared to a Tax agent are the services that can be provided for income tax. For example, A BAS agent cannot provide services relating to income tax matters such as:

- discussing on your behalf, matters relating to Tax Agent services with the ATO

- preparation and lodgment of Income Tax returns, Fringe Benefits Tax (FBT) returns

- varying Pay as You go Instalments and FBT Instalments that appear on a Business Activity Statement

- providing technical advice on matters of Income Tax or FBT legislation.5

If a BAS agent is found to be providing Tax Agent services for a fee then there are extreme penalties if they are clearly not registered as a Tax Agent with the Tax Practitioners Board. Consequences of non-compliance are explained shortly.

The ATO provides clear examples of BAS agent services and Tax agent services.

What they need to know and do for their clients

To effectively process and complete business activity statements and instalment activity statements, an agent needs to be competent in the following:

- relevant legislation knowledge

- GST terminology and appropriate application to financial transactions

- GST regulations, obligations and Australian Taxation Office requirements

- specific taxation requirements for business purposes

- taxation parameters

- accounting terminology relevant to the industry

- Australian taxation requirements

- evidence of the ability to maintain accounting records for a variety of business types for taxation purposes

- accurately complete all sections of both Business Activity Statements and Instalment Activity Statements for multiple entity types.

Tasks carried out for the completion of activity statements and worksheets follow.

- Differentiating the various types of inputs and outputs that are required to be reported on the statements for the ATO.

- Demonstrating the application of information to the GST worksheet with particular attention to whether the enterprise is an accruals or cash payer.

- Preparation of worksheets and including FBT and PAYG, including calculation of PAYG instalment amounts using the ATO percentage and gross income net of GST.

- Calculating the amounts of LCT and WET that may be required to be reported to the ATO

- Demonstrating the application of GST to capital purchases and their treatment on the business activity statement

- Preparing the business activity and instalment activity statements for timely lodgment with the ATO.

Examples of BAS services

This table includes a non-exhaustive list of services that may and may not constitute a BAS service under the TASA.

| Service | BAS service | Not a BAS service |

|---|---|---|

| Applying to the Registrar for an ABN on behalf of a client. | X | |

| Installing computer accounting software without determining default GST and other codes tailored to the client. | X | |

| Coding transactions, tax invoices and transferring data onto a computer program for clients through processes that require the interpretation or application of a BAS provision. | X | |

| Coding transactions, tax invoices and transferring data onto a computer program for clients through processes that do not require the interpretation or application of a BAS provision. | X | |

| Confirming figures to be included on a client's activity statement. | X | |

| Completing activity statements on behalf of an entity or instructing the entity which figures to include. | X | |

| General training in relation to the use of computerised accounting software not related to client's particular circumstances. | X | |

| Preparing bank reconciliations. | X | |

| Entering data without involvement in or calculation of figures to be included on a client's activity statement. | X | |

| Providing advice about or confirming the withholding tax obligations for the employees of a client. | X | |

| Services declared to be a BAS service by way of a legislative instrument issued by the TPB. | X | |

| Preparing and providing an income statement that may include reportable fringe benefits amounts and the reportable employer superannuation contributions. | X | |

| Registering or providing advice on registration for GST or PAYG withholding. | X | |

| Services under the Superannuation Guarantee (Administration) Act 1992 to the extent that they relate to a payroll function or payments to contractors. | X | |

| Advising about an SGC liability, including calculating the liability and preparing the SGC statement | X | |

| Advising about the offsetting of late payments of superannuation contributions against the SGC | X | |

| Completing the late payment offset election section of an SGC statement | X | |

| Representing a client in their dealings with the ATO relating to the SGC – lodging SGC statements, being an authorised contact relating to SG and SGC, and accessing these accounts in the ATO's online services for BAS agents | X | |

| Being an authorised contact with the ATO for payment arrangements relating to SGC account | X | |

| Being an authorised contact with the ATO for requesting penalty remissions relating to SGC | X | |

| Being an authorised contact for any audit or review activity undertaken by the ATO relating to SGC | X | |

| Advising about claiming of an allowable tax deduction for superannuation contribution | X | |

| Advising about superannuation contribution caps and the effect of exceeding those caps | X | |

| Advising on salary sacrificing arrangements and salary packaging | X | |

| Advising about fringe benefits tax laws | X | |

| Advising about, preparing and/or lodging income tax returns | X | |

| Determining and reporting the superannuation guarantee shortfall and associated administrative fees. | X | |

| Dealing with superannuation payments made through a clearing house. | X | |

| Completing and lodging the Taxable payments annual report to the ATO on behalf of a client. | X | |

| Sending a TFN declaration to the Commissioner on behalf of a client. | X | |

| Transmitting data to the Commissioner through single touch payroll (STP) enabled software, where the data transmission does not require the interpretation or application of a BAS provision. | X | |

| Providing a payroll service that interprets and applies a BAS provision, including reporting employee payroll information through STP-enabled software. | X | |

| Undertaking a payroll compliance review, providing an assessment or opinion on whether the client is compliant with one or more BAS provisions. | X | |

| Determining eligibility, providing advice, and assisting eligible clients in electing to participate in the JobKeeper Payments scheme. | X | |

| Determining eligibility, providing advice, and assisting eligible clients about their Cashflow boost entitlements. | X | |

| Determining eligibility, providing advice, and assisting eligible clients in claiming the JobMaker Hiring Credit. | X |

Examples of tax agent services

This table includes a non-exhaustive list of services that may or may not constitute a tax agent service under the TASA if provided for a fee or reward.

| Service | Tax agent service | Not a tax agent service |

|---|---|---|

| Preparing returns, notices, statements, applications or other documents about your client's liabilities, obligations, or entitlements under a taxation law. | X | |

| Lodging returns, notices, statements, applications or other documents about your client's liabilities, obligations, or entitlements under a taxation law. | X | |

| Assisting clients with tax concessions for expenditures incurred on research and development activities where the service involves the application of taxation laws. | X | |

| Preparing depreciation schedules on the deductibility of capital expenditure. | X | |

| Preparing or lodging objections on behalf of a taxpayer under Part IVC of the Taxation Administration Act 1953 (TAA) against an assessment, determination, notice or decision under a taxation law. | X | |

| Giving clients advice about a taxation law they can reasonably be expected to rely on to satisfy their taxation obligations. | X | |

| Dealing with the Commissioner on behalf of clients. | X | |

| Applying to the Commissioner or the Administrative Appeals Tribunal (AAT) for a review of, or instituting an appeal against, a decision on an objection under Part IVC of the TAA. | X | |

| Reconciling BAS provision data entry to ascertain the figures to be included on a client's activity statement. | X | |

| Filling in an activity statement on behalf of a client or instructing them which figures to include. | X | |

| Ascertaining the withholding obligations for employees of your clients, including preparing income statements. | X | |

| Installing computer accounting software and determining default goods and services tax (GST) and other codes tailored to clients. | X | |

| Installing computer accounting software without determining default GST and other codes tailored to clients. | X | |

| Coding transactions, particularly in circumstances where it requires the interpretation or application of a taxation law. | X | |

| Coding tax invoices and transferring data onto a computer program for clients under the instruction and supervision of a registered tax or BAS agent. | X | |

| Contracting the services of a specialist to provide advice about an area of taxation law that you have no expertise and cannot review for accuracy. | X | |

| Services provided by an auditor of a self-managed superannuation fund under the Superannuation Industry (Supervision) Act 1993. | X | |

| Providing general taxation advice to clients that does not involve applying or interpreting a taxation law to the client's personal circumstances. | X | |

| General training (such as a classroom) in relation to the use of computerised accounting software not related to particular fact situations. | X | |

| Preparing bank reconciliations. | X | |

| Entering data. | X | |

| Providing a payroll service that involves interpreting and applying a taxation law, including reporting employee payroll information through single touch payroll (STP) enabled software. | X | |

| Undertaking a payroll compliance review, providing an assessment or opinion as to whether the client is compliant with their taxation obligations under one or more taxation laws. | X | |

| Providing tax related advice specific to client's circumstances regarding: PAYG withholding liability, Superannuation Guarantee obligations, fringe benefits tax laws, and termination and redundancy payments. | X | |

| Transmission of data to the Commissioner through single touch payroll (STP) enabled software, where the data transmission does not require the interpretation or application of a taxation law. | X |

Service Checklist

A service checklist can help clarify your client's current business needs and identify future requirements. Once you have this information, you can use it to assist you in creating a referral list for your clients. Your service checklist is not a static document. It will need to be updated as your business evolves.

Activities

1. Download thissample service checklistword documentand review the services shown and questions for discussion with your client before continuing with the video below.

In this video, Andrew LaCivita speaks about business networking and how to build professional relationships.

2. Review the table at the ATO website that describes examples of BAS services and then answer the questions that follow to confirm your understanding.

BAS provision

The term ‘BAS provision’ is defined in the Income Tax Assessment Act 1997 as:

- Part VII (collection and recovery only) of the Fringe Benefits Tax Assessment Act 1986

- the indirect tax laws, including

- the goods and services tax (GST) law

- the wine tax law

- the luxury car tax law

- the fuel tax law, and

- Parts 2-5 and 2-10 in schedule 1 of the Tax Administration Act 1953, which are about the pay as you go (PAYG) system

Accountant

This role has a much broader scope than a Bookkeeper or Tax Agent. They analyse and interpret financial records in order to identify problems or opportunities for the business to perform better. An Accountant can only perform tax-related advice and complete tax returns if they are a Registered Tax Agent. They can also act as BAS agents if they are Registered Tax agents, but their time may be better spent providing analysis and advice.

With the rise of technology and automation tools, the role of accountants is shifting. Accountants and CFOs are working more and more on strategy, analysis, and decision-making for businesses. However, they also manage taxes for companies and individuals. They use the profit & loss statement, balance sheets, and income statements to provide an overview of a business's financial health.6

In addition to Accountant and CFO, typical mainstream job titles include:

| Finance Director | Chief accountant |

| Financial Controller | Management Accountant |

| Financial Analyst | Cost Accountant |

| Treasurer | Internal Auditor |

| Chief Information Officer | Compliance Officer |

| Investor relations officer | Project Manager |

| Strategy analyst | Commercial Manager |

The table below further explains the differences between the roles.

| Bookkeeper | BAS Agent | Tax Agent | Accountant | |

|---|---|---|---|---|

| Credentials |

No formal education is required. Must have:

Often these skills are acquired through completing a Certificate IV in Accounting and Bookkeeping qualification. |

If providing BAS services for a fee or other reward they must be registered by the Tax Practitioners Board (TPB). These are the qualifications and experience requirements set out by the ATO website for BAS agents. |

If providing BAS or Tax services for a fee or other reward they must be registered by the Tax Practitioners Board (TPB). These are the qualifications and experience requirements set out by the ATO website for Tax agents.You will see they are robust.

|

Formal qualification - bachelor's degree in accounting or finance. |

| Functions |

Bookkeepers record and manage the daily financial transactions of a business. This includes:

|

May include those of Bookkeeper and assists with BAS statement preparation and lodging. Must abide by the TPB Code of Professional Conduct. |

May include those of Bookkeeper and assist with BAS statement preparation and lodging. Authorised to charge for tax advice and lodge tax returns. Must abide by the TPB Code of Professional Conduct. |

Accountants provide financial analysis on data that a bookkeeper has entered. This includes:

|

| Documents prepared |

Bookkeepers prepare:

|

|

|

Accountants may prepare and lodge everything a tax agent can do, however normally they focus on strategy and direction. |

| Reporting Obligations |

Bookkeepers may lodge:

|

BAS agents may lodge

|

Tax agents may also lodge

|

Accountants that are also Tax agents may lodge:

|

| Professional Certification |

Bookkeepers can become members of:

|

Must be registered with the ATO and may become members of those of a bookkeeper and:

For a complete list visit the ATO resource. |

Must be registered with the ATO and may become members of those of a bookkeeper, BAS agent and:

For a complete list visit the ATO resource. |

Certified Accountants can become members of all of the associations previously mentioned and:

|

Failure to comply risks consequences

Failing to comply with the Relevant Australian Taxation Office (ATO) and Tax Practitioner Board (TPB) requirements, including TPB registration requirements and the Code of Professional Conduct, could result in civil penalty provisions and/or administrative sanctions.

The issues are separated into two categories.

- Conduct that is prohibited without registration

- Conduct of registered BAS agents

A civil penalty is a financial penalty in a civil rather than criminal jurisdiction. State and Commonwealth government bodies can apply to the courts to have a fine imposed against an entity for breaching a civil penalty provision in some circumstances.

Civil penalties do not include criminal convictions or imprisonment.

The Federal Court has the power to impose penalties of up to $55,500 for individuals and $277,500 for corporations for each breach.

Additional information can be found on these TCB websites:

The government runs several bodies that support, regulate, and oversee the people and activities involved with paying taxes in Australia.

Organisations

The Tax Practitioners Board (TPB)

The TPB is responsible for the registration and regulation of all tax agents, BAS agents and tax (financial) advisers (collectively referred to as “tax practitioners”) in Australia. The TPB is also responsible for ensuring compliance with the Tax Agent Services Act 2009 (Cth) (TASA), including the Code of Professional Conduct (Code).

This is achieved by:

- administering a system to register tax practitioners, ensuring they have the necessary competence and personal attributes;

- Providing guidelines and information on relevant matters

- investigating conduct that may breach the TASA, including non-compliance with the Code, and breaches of the civil penalty provisions

- imposing administrative sanctions for non-compliance with the Code

- applying to the Federal Court about contraventions of the civil penalty provisions in the TASA.

The TPB consists of a Board and Chair appointed by the Minister for Revenue and Financial Services and staff made available by the Commissioner of Taxation.7

Australian taxation office (ATO)

The ATO is the Australian Government’s principal revenue collection agency. The ATO delivers various social and economic benefit and incentive programs administers significant aspects of Australia’s superannuation system and acts as custodian of the Australian Business Register.8

The ATO is the final word on current tax laws and legislation. The website is divided into categories, and each area contains extensive current information.

Let's examine the ATO website resource:

This screenshot of the ATO's landing page provides several avenues of information. To view the services behind each of the tabs shown above, you must set up an account with the ATO. You will be prompted to log in before gaining access. Help services can be accessed by hovering over any of the tabs and selecting a link from the menu that appears, as shown in Not-for-profit below.

- Business portal

- Not-for-profit tab

- Super tab

- Tax professionals tab

- Keyword search

- General info based on tax season

- Chat support

1. Business Portal

This section allows businesses to register with the ATO, lodge BAS and IAS, manage payments and reporting, stay current with tax tables, download forms, and manage reporting for PAYG and Super.

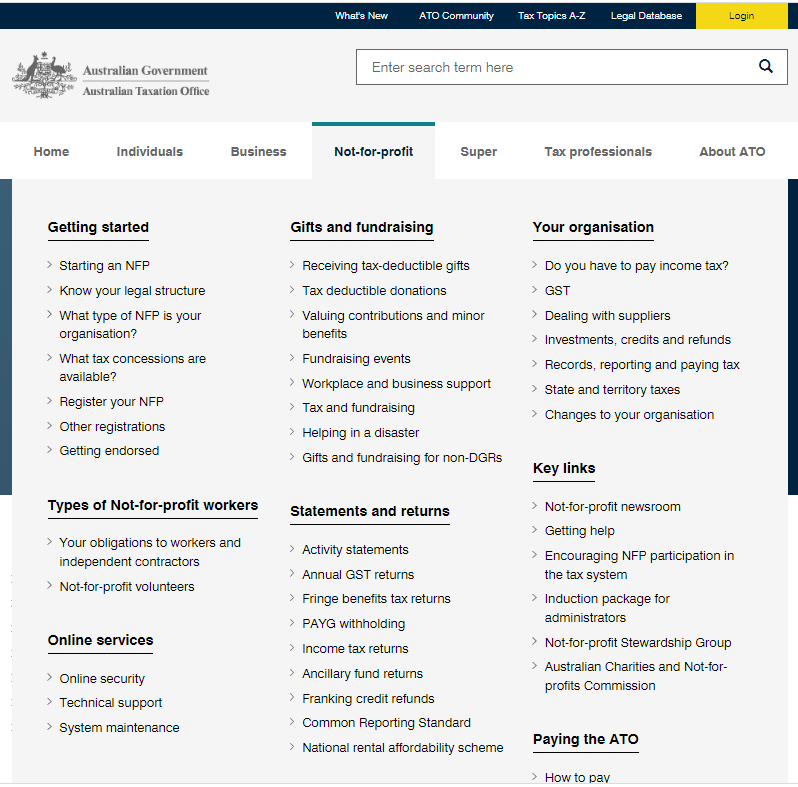

2. Not-for-profit tab

This section is for those businesses that don't need to collect GST because they are a recognised charity organisation. You can see by the screenshot below how many topics the ATO provides for assistance.

3. Super tab

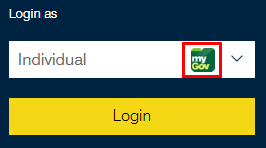

Paying and tracking super payments can be challenging. You can find information about individuals, employers, online services, and various super funds. If you log in as an individual (for any of the tabs), you will be allowed to link ATO's portal with a myGov account.

4. Tax professionals tab

This section allows tax professionals and BAS agents to prepare and lodge on behalf of clients, use the ATO's digital services, and pay the ATO.

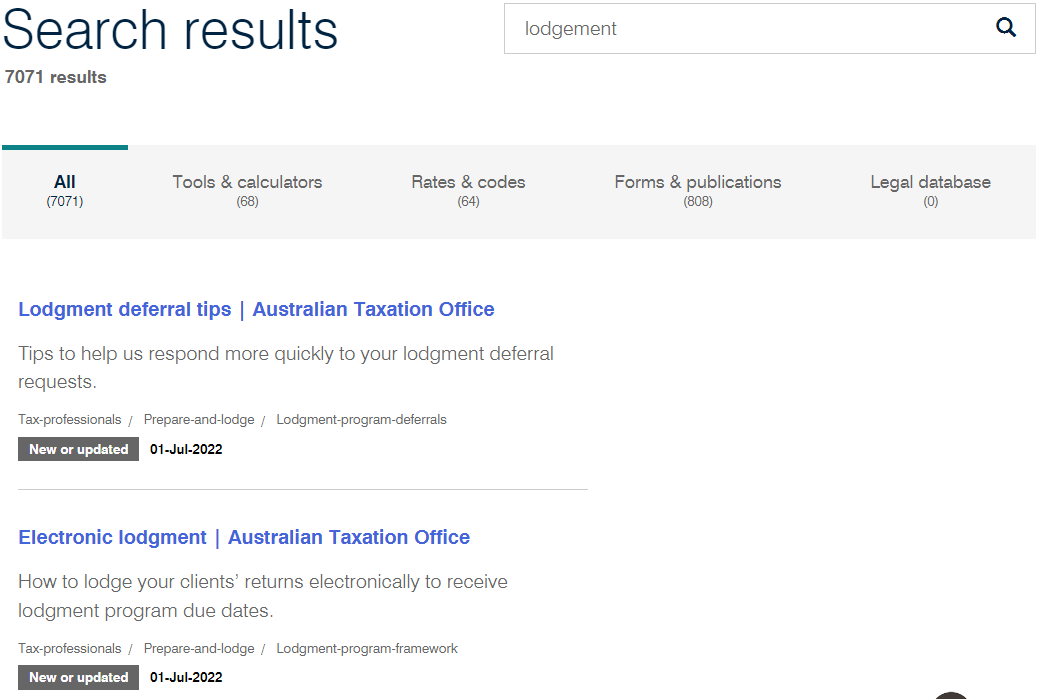

5. Keyword search

Direct navigation will be more straightforward, but in a pinch, enter a keyword. Your results will be broken down into categories, with new or updated information near the top of the results, as shown here:

6. General info based on tax season

When you land at the ATO, you can immediately access any number of valuable articles below the main image and login field.

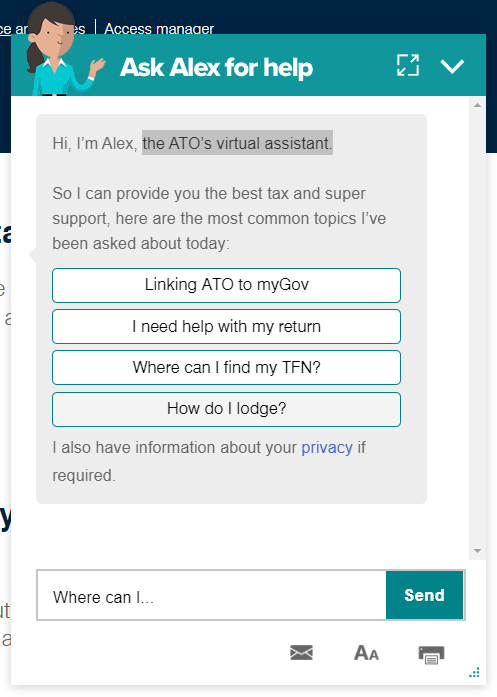

7. The chat support prompt, Alex

The ATO has brought on Alex, the ATO’s virtual assistant. You can always reach out by initiating a chat with Alex or selecting from the list of frequent support requests.

return to ATA Screenshot

return to list

The Australian Charities and Not-for-profits Commission (ACNC)

The ACNC is the national regulator of charities and was established in December 2012 to achieve the following objectives:

- maintain, protect and enhance public trust and confidence in the Australian not-for-profit sector

- support and sustain a robust, vibrant, independent and innovative not-for-profit sector

- promote the reduction of unnecessary regulatory obligations on the sector.9

What the ACNC does

- It registers organisations as charities.

- It helps charities understand and meet their obligations through information, guidance, advice and other support.

- It helps the public understand the work of the not-for-profit sector through information, guidance, advice and other support.

- It maintains a free and searchable public register so that anyone can look up information about registered charities.

- It works with state and territory governments (as well as federal, state and territory government agencies) to develop a 'report-once, use-often' reporting framework for charities.

Knowing the lingo is part of any profession. Accounting and bookkeeping rely on many abbreviations and we've provided a list below. Before you look at it, take a quiz to see how many you already know.

The following abbreviations have been provided as they will be referred to throughout the discussions in this unit and are key terms when working with business activity statements.

| Abbreviation | Stands for |

|---|---|

| ABN | Australian Business Number |

| ABR | Australian Business Register |

| ACCC | Australian Competition And ConsumerCommission |

| ANTS | A New Tax System |

| ASIC | Australian Securities and Investments Commission |

| ATO | Australian Taxation Office |

| BAS | Business Activity Statement |

| BSP | Bas Service Provider |

| CAP | Capital Purchase |

| CTP | Compulsory Third Party (Insurance) |

| FBT | Fringe Benefits Tax |

| GIC | General Interest Charge |

| GNR | GST Not/Non Registered |

| GST | Goods And Services Tax |

| GW | Consolidated WET And WEG |

| FRE | GST Free |

| AIS | Instalment Activity Statement |

| IMP | Import Duty |

| INP | Input Taxed |

| ITAA | Income Tax Assessment Act |

| ITC | Input Tax Credit |

| LCT | Luxury Car Tax |

| NAT | Unique Number Allocated To ATO Form |

| PAYG | Pay As You Go |

| RCTI | Recipient Created Tax Invoice |

| SBE | Small Business Entity |

| TFN | Tax File Number |

| TPB | Tax Practitioners Board |

| WEG | Wine Equalisation Tax [WET] Plus GST |

| WST | Wholesale Sales Tax |

| WET | Wine Equalisation Tax |

The ATO is an excellent resource for businesses that are just getting started. Take a look at the options, and put yourself in the shoes of a person hired to help a fledgling business set up its financial and reporting structure.

Activity: Watch the video about Activity Statements on the ATO website, answer a few questions about the knowledge you gained from watching it and then pick a few videos from their series from the titles that interest you.

- Watch the video: Activity Statements

- Pick at least 2 more from their video series: Tax basics for small business video series.